Volatility - Sticky strike vs Sticky delta

Understanding the sticky delta and sticky strike rules for volatility will help us determine how the volatility skew changes when the markets move.

The sticky strike rule:

Some market players believe that when the stock/index moves, the volatility skew for an option remains unchanged with strike. This behaviour is referred to as the the sticky strike rule. The rule is appliacable when the markets are expected to range bound in near future without significant change in realized volatility.

The sticky delta rule:

There are some market players that tend to believe that the volatility skew remains unchanged with moneyness. For example lets say that the implied volatility for an ATM option is 30% with the index leve being at 100. Now if the index declines to 90, this rule would predict that the implied volatility for 90 stike option would now be 30%. Hence the behaviour is known as sticky moneyness or sticky delta.

The sticky delta rule is more applicable when the markets are trending without a significant change in realized volatility.

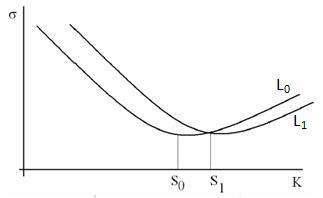

The Figure 1 below shows figuratively how the volatility skew gets affected under the two rules. If the current level of the underlier was S0 and the volatility skew for a specific tenor was indicated by L0. Under the sticky strike rule, the skew remains the same L0. Under the sticky delta rule the skew moves in the direction of the underlier move. Thus when the underlier moves from S0 to S1, the new skew is indicated by L1.

figure 1:Volatility skew as the market moves

Both the sticky strike and sticky delta rules have been proven to provide arbitrage oppportunities. However, these rules do help us understand the risks of the traded products.

It is known that when the market falls, the impied volatility is observed to increase. E. Derman describes a sticky implied tree rule which is consistent with this observation and is also argued to be arbitrage free.

Reference

[1] Regimes of volatility, Quantitative Strategies Research Notes, Emanuel Derman.