Managing risks of Digital payoffs - Overhedging

When a new trade comes to the risk manager in a bank for approval, he tries to determine both the quality and the quantity of the risks inherent in the trade. If he's not comfortable with either of the two, he may not approve it. Some of the factors that are considered are:-

1. Whether the bank has a model to price and determine the risk of the trade. (And yes it happens, with virtually any payoff possible in the OTC equity derivatives markets, the bank will not always have the model to handle the trade).

2. Number of underliers to the trade and whether these underliers are liquid indices or thinly traded stocks. Managing the risks of a multi asset trade with illiquid stocks as undeliers would be the most difficult.

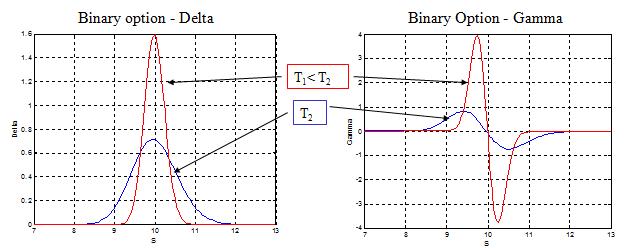

3. Discontinuities in the payoff. The greeks-delta and gamma in general as the spot approaches the barrier become extremely volatile. With a standard digital option, everytime the spot moves over/below the strike, there would be a need to rebalance the hedges.

Ofcourse, Not all trades require pre approval esp. ubiquitous trades like single asset cliquets, autocallables, CYNs etc. whose risks have been studied and researched well generally do not require approval. For new payoffs the trader will come up wth an overall hedging strategy for the trade. Often the most important aspects of the hedging strategy revolves around managing greeks around discontinuities (or barriers). In this article, I shall talk about 'Overhedging' which is a technique to handle effectively risks around barriers.

The following daigram shows the delta and the gamma for the digital option.

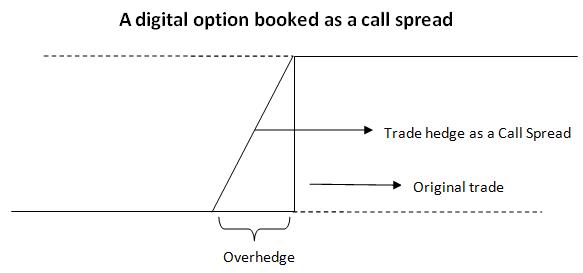

Overhedging - Barrier/Digital options hedged as option spreads

Almost always a barrier/digital options are booked and hedged as option spreads. What the trader achieves by doing so is a smoother set of greeks specially the delta. As an example let's consider a binary option in the figure below booked as a call spread.

It's important to note that the call spread is structured that it is more expensive than the original binary option. What this means is that when a buyer comes to a bank with a price request for a digital option, the bank actually quotes price for a call spread. To summarise a digital option is hedged as a call spread with a long position on a call with "strike = strike of the digital - overhedge amount" and a short position on a call with "strike = strike of the digital" with each with a quantity = "the digital payoff/overhedge". The overhedge amount is normally fixed at a level 3-8% of the digital payoff level.

It's easy to see that the maximum delta for this call spread will be "Digital payoff/Overhedge amount".

To extend the discussion to the barrier trades, a barrier trade can be viewed as a combination of an option spread and an option. For example an up and in call option can be booked and hedged as a combination of a call spread (with strikes being barrier and barrier - overdhedge) and a call option with strike equal to the barrier level.